Adam Copeland and Owen Engbretson

The Federal Reserve’s 2022-23 tightening cycle includes the use of two monetary policy tools: changes in policy rates and changes in the size of its balance sheet. This post highlights the results of a recent Labor Report that examines how these instruments affect financial market conditions. Using trade-level private data, we find that both instruments have significant effects on the prices of repo-acquired funds. These results suggest that the Fed can control how and when monetary conditions affect economic conditions. For example, the Fed can reduce its policy rates to reduce economic conditions, while reducing its rate to maintain liquidity in the stock market.

Rear end

Our analysis focuses on repurchase agreements (repo), an important financial market used to save funds and provide funds, with an estimated balance of more than $ 5 trillion remaining in the first half of 2024 (see the appendix of this white paper). Secured US financial transactions are often labeled as repos, and within a repo, transactions related to Treasury securities are dominant. Using data on the Treasury repo, then, provides a proxy for looking at the US’s safe financial position

The US Treasury’s Office of Financial Research’s (OFR) central bank repo collection provides such information. This collection is winning many tradesmen. In addition, a portion of seller-to-buyer repo transactions are collected through a service program sponsored by a central company, which provides information on trade prices between dealers and their mutual fund and hedge fund clients (see Staff Report for more details on Sponsored Service).

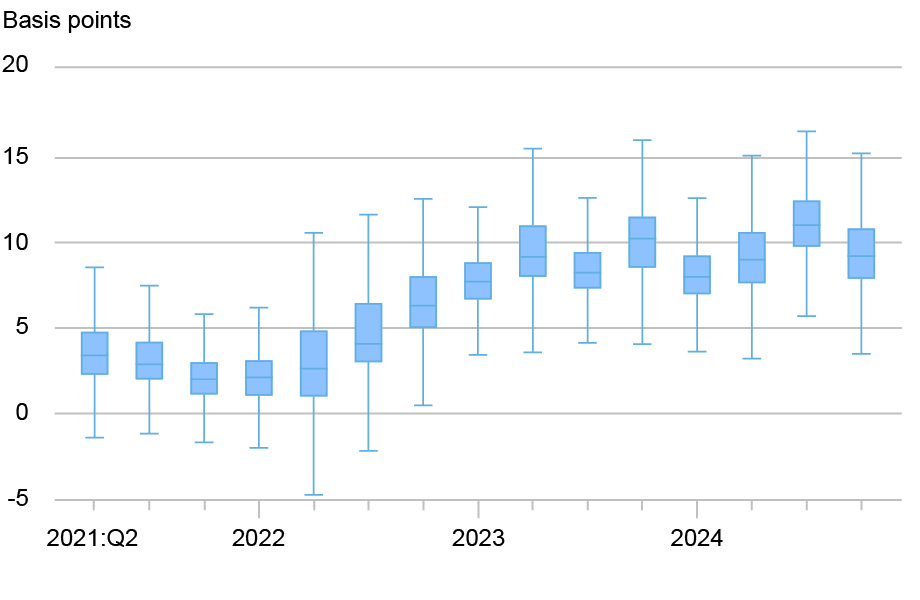

Brokers are key intermediaries in securities markets, borrowing from wealthy investors such as stock market mutual funds and lending to leveraged customers such as hedge funds (see this full report on broker-dealer activities). The OFR data allows to build the profits charged by dealers to intermediate funds, while we see the charge of repo dealers to lend money to the charged customers as well as the fees paid to borrow funds from the syndicates. The chart below shows the distribution of those estimates for the overnight Treasury repo for each quarter from 2020 to 2024.

Distribution of Paid Advertising by Dealers, Quarterly

Notes: This chart is a box-and-whisker plot of the total daily fees charged by brokers to broker-dealers per quarter. The spread is calculated as the rate charged by dealers to lend money to customers on the overnight Treasury repo minus the rate paid by dealers to borrow money from customers on the overnight Treasury repo. The three box lines represent the 25th, 50th, and 75th percentiles of the daily average. The lower limit is equal to the 25th percentile minus 1.5 times the interquartile range (75th minus 25th percentiles). The upper beard is described in the same way. The project does not include external value.

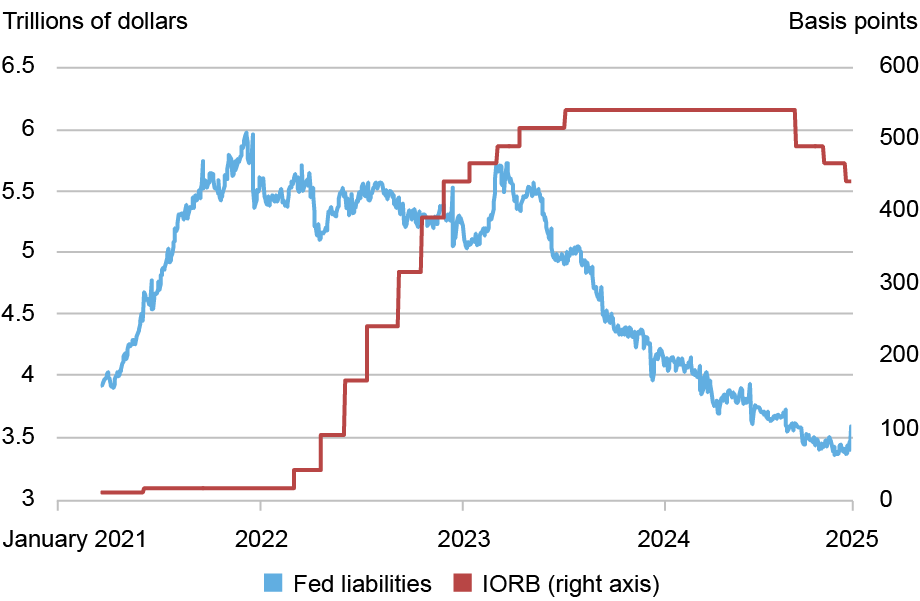

These statistics suggest that traders have charged a widening flow in the middle funds by tightening monetary policy, which began in March 2022. The chart below shows changes in monetary policy, based on changes in the Fed’s operating rate on reserve balances (IORB) and on the Fed’s balance sheet (our measure of the Federal Reserve’s money is the amount of money the bank holds on reserve. Federal Reserve overnight reverse repo facility, then Fed liabilities). During the sample period, the IORB increased from 15 to 540 basis points, with major steps in 2022. At the end of the sample, the last half of 2024, there are three decreases in the IORB. Fed loans have the shape of a hump: Starting at about $4 trillion, they rise exponentially by 2021 to $6 trillion. They then remain flat from the beginning of 2023, before gradually declining through 2024, reaching $3.5 trillion in December 2024.

Changes in Monetary Policy during the Model Period

Notes: This chart shows the growth of the IORB and the size of the Federal Reserve’s liabilities as measured by the amount of bank deposits at the Federal Reserve Banks as well as the amount on deposit at the Federal Reserve’s overnight reverse repo facility.

Analysis

Our analysis focuses on how monetary policy affects costs to sellers and intermediate funds among consumers. As intermediaries, brokers face risks, even for short-term trades where funds are secured by high-quality collateral (see this Treasury Market Practices Group white paper for a distillation of these risks). To reduce these risks, sellers often have water buffers, where the cost of maintaining this buffer must be shown in the declaration paid by the seller.

We call this fee the “liquidity risk premium” and we recognize that this fee should vary according to the opportunity costs of holding money. Changes in monetary policy, both according to the IORB and Fed bills, change the opportunity cost of holding money. Therefore, our primary exercise is to estimate how changes in the IORB and Fed rates affect the flow charged by traders to intermediate funds. The idea that distinguishes this analysis is that the decision to change rates or loans of the Fed comes from the announcements paid by sellers, which is a reasonable idea for this period of analysis when the Money wants to go from more sources to more.

Our main results are that a second increase in the IORB or a decrease in the Fed’s lending rate raises the credit risk premium, raising the cost of intermediate funds. Estimates suggest that a one standard deviation increase in IORB, or 226 points, raises the credit risk premium by 2.1 to 3.5. A one-sided increase in Fed borrowing ($750 billion) lowers rates by 1.6 to 2.5. These are important economic implications, as evidenced by the fact that the average distributor charges consumers an average of 7.5 basis points during the sample period.

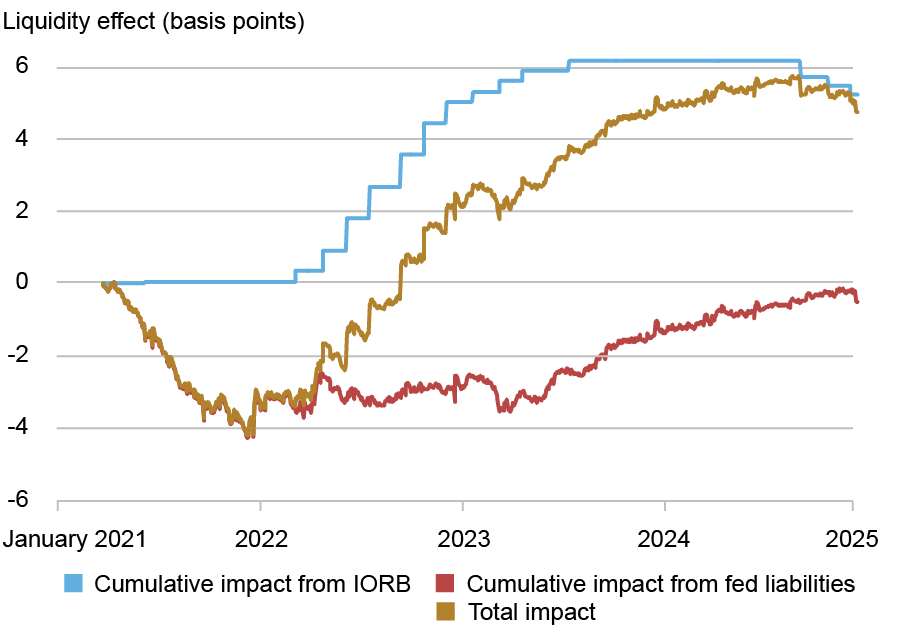

An overview of each monetary policy instrument in credit risk assessment is shown in the chart below. The estimated effects naturally reflect their monetary policy instruments, although the magnitude varies slightly due to the estimated effects. For example, a $1 billion change in Fed loans has a larger estimate of the credit risk premium when IORB is low compared to when IORB is high.

Estimating the Incremental Effect of Monetary Policy on the Liquidity Risk Premium

Notes: This chart shows the overall effects of monetary policy on the credit risk premium as inferred from the estimated results, where the effects are set to zero at the beginning of the sample. A decomposition is also provided, separately showing the effect of changes in IORB and Fed debt on the credit risk premium.

Take away

In the past period of monetary tightening, the Fed’s increase in the IORB and the reduction in Fed borrowing both raised the cost of money, raising the credit risk premium. An important takeaway from the results is the potential for a wide variety of outcomes in how the Fed affects money markets. For example, in a hypothetical situation where the economy needs support and the level of interest rates in the financial sector is about, the Fed has tools available to solve both problems: lowering the interest rate and reducing its debt. Low interest rates will boost the economy through normal channels, and a large enough reduction in Fed debt could result in the spread of spreads charging consumers in the medium term, weakening the overall financial sector. We can measure the effects on the liquidity risk premium. Using the value of Fed rates and liabilities at the end of the sample period, our results suggest that a 100 basis point reduction in the IORB and a reduction of $400 billion in Fed liabilities would have significant effects on the credit risk premium.

Adam Copeland is a financial research consultant at the Federal Reserve Bank of New York’s Research and Statistics Group.

Owen Engbretson is a research analyst at the Federal Reserve Bank of New York’s Research and Statistics Group.

How to cite this post:

Adam Copeland and Owen Engbretson, “The Fed has two tools to influence stock market conditions,” Federal Reserve Bank of New York. Liberty Street EconomicsApril 6, 2026, https://doi.org/10.59576/lse.20260406

BibTeX: See |

Freedom

The views expressed in this post are those of the author and do not necessarily reflect the position of the Federal Reserve Bank of New York or the Federal Reserve System. Any errors or omissions are the responsibility of the author(s).

#Fed #tools #influence #financial #market #conditions #Liberty #Street #Economics