Economic Facts

As the market continues to move higher on Wednesday, lifting long-term highs in the Pro Portfolio stock along with the bulk of the newly updated EPS Diplomats basket, it would be a mistake to take our eyes off today’s March data.

This collection is the first hard look at what has been captured, captured, or whatever you want to call it, since the beginning of the US-Iran conflict, and the proliferation of oil, gas, diesel and other things that we have been traveling with you for the past few months.

ADP’s March Employment Change Report

ADP found that US private businesses added a total of 62,000 jobs in March, adding to the 66,000 revised in February and exceeding market expectations for an increase of 40,000. Taking a closer look at the data from the next three months, we see an upward slope in the pace of job creation to ~46K from ~39K in February and ~8K in January.

By itself, that does not indicate a strong job creation situation, but it is not an unsustainable situation. And that’s not enough to motivate the Fed to cut rates, especially based on what we’re going to talk about in the next two parts.

S&P Global’s Final March Manufacturing PMI

The final findings from S&P are no different than those found in its Flash report, and what we see is a pick-up in manufacturing activity in March, and an increase in new and structured activity. However, that activity appears to be more driven by potential safety stockpiling given the US-Iran related topics than actual demand.

Job creation was weak in the manufacturing sector during March, but as we expected, higher electricity prices led to higher fuel prices, while tariffs continued to increase costs. As S&P put it:

“Overall prices rose sharply, and inflation rose to its highest level since last August. Wherever possible, factories increased their prices due to increased input costs. Factory-gate prices rose at a noticeable pace in March, and inflation hit a seven-month high.”

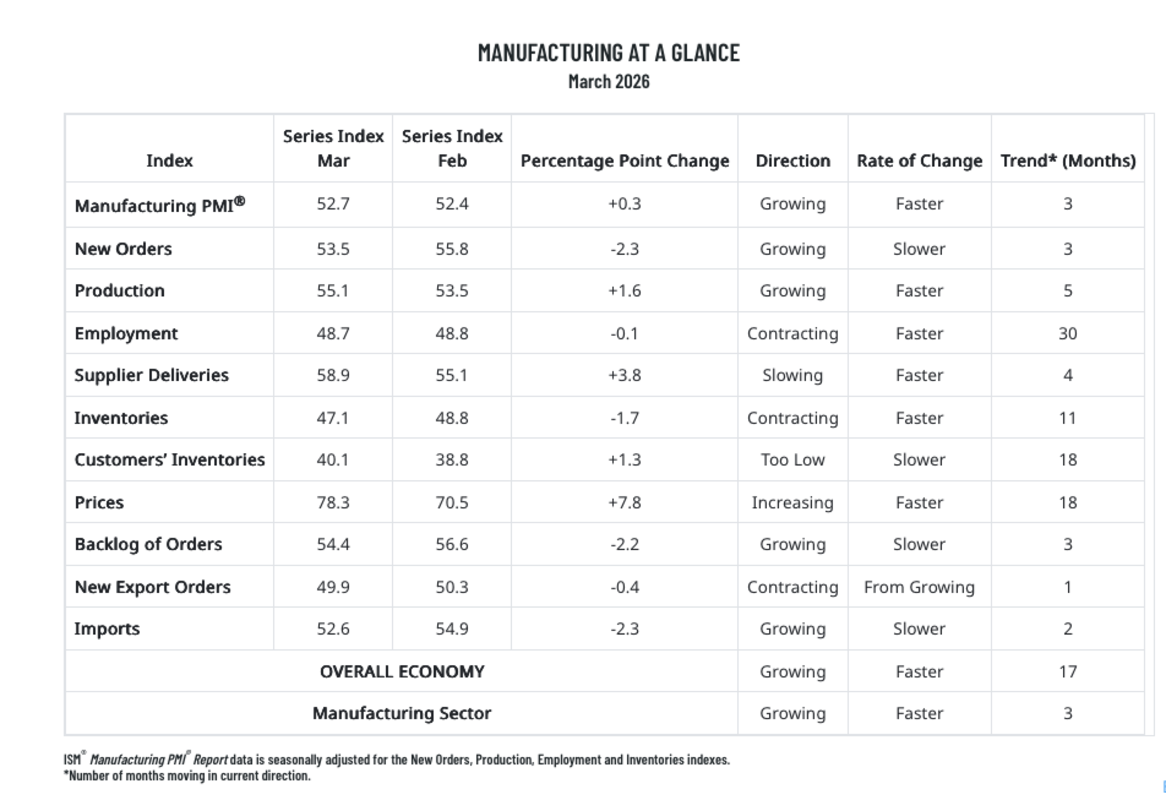

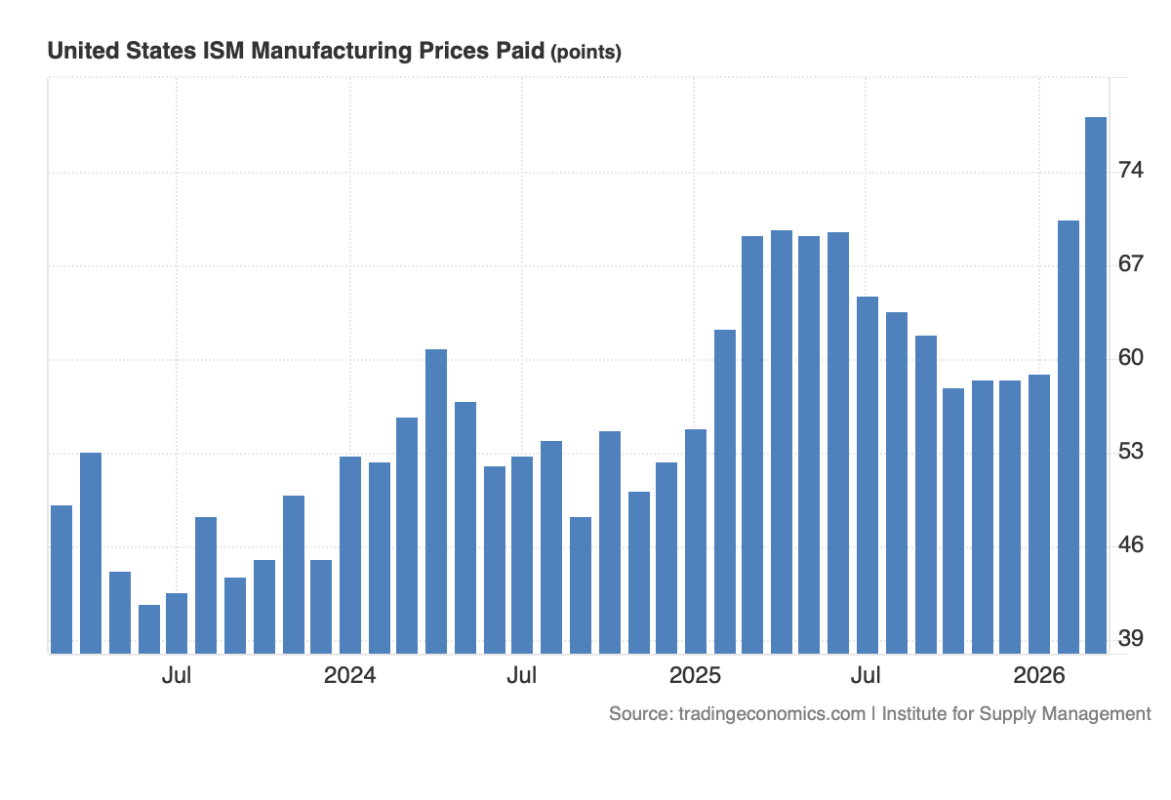

ISM’s March Manufacturing Index

Most of the March manufacturing PMI data released by ISM is similar to that from S&P Global, but it is hard to miss the slight jump in the Price index to 78.3.

To put some perspective around it, let’s look at where that indicator has been over the past three years.

What about February Sales?

January headline Retail & Food Service sales increased to 3.7% year-on-year, up from 3.2% in February and 3.1% for the period December 2025-February 2026 on the same basis. Looking at Retail alone, that spending has increased by 3.5% compared to March 2025, and when we read the data, we find that the spending barometer was the fastest during the following three months.

Where we saw upticks in the reporting segments were apparel, sporting goods and related areas, automobiles, and food service/restaurants. The data showed a decline in spending on furniture, department stores, gas stations and grocery/food and beverage stores. We are also seeing slower consumption in building materials and general merchandise stores.

Our take on this suggests our position on TJX Cos. (TJX) and we continue to see it in good shape as consumers struggle with higher gas and other prices. Remember in today’s opening remarks, we discussed the impact of higher oil, gas and diesel prices on food delivery costs.

And although it seems like almost forever ago now, at Costco (CLAIMS) reported its latest quarter, including its February sales comp. Adjusted US comps sales rose 6.0% in February compared to March’s 0.2% decline for grocery stores, and a 1.2% gain for general merchandise stores, and a 3.5% year-over-year increase in Retail sales. While it may be a bit in the rear-view mirror and Costco is set to release its March sales report on April 8, it’s still a good bit of confirmation for Costco continuing to win share of the consumer wallet.

Putting It All Together

While collecting the above components, let’s remember that the manufacturing economy is responsible for 10%-15% of the GDP, and the service economy is accumulating money. Between the ADP jobs numbers for March and the ISM numbers that are still contracting in March, we will want to see an upward step in the ISM employment indicators when the report is released on Monday (April 6). It will be behind this Friday’s August Employment Report, which will be released during the market holiday, but the ISM data will help us better understand where jobs are being created.

Both S & P Global and ISM find a strong increase in inflationary pressures – again, not all that surprising – we may see a combination of renewed inflationary pressures from March, April, maybe May CPI and PPI data. That will depend, as we’ve said, on where energy and related prices sit in the coming weeks and months, but we’re likely to see margin pressure emerge when companies report their March quarter results.

Due to the renewed pressure on inflation, which will reduce consumer spending, we should expect to see several units in the monthly report of Retail Sales decrease in March compared to February. That will make us very interested in comparing that March report against Costco’s March sales report. Based on our trips to Costco in March, even if Costco continues to make strong numbers for 2025, we should see a good comp for good sales.

We should also expect that unsold retail sales in March will exceed other categories, especially thanks to Amazon. (AMZN) March 25-March 31 Big Spring Sale. Yes, we continue to see shoppers flock to Amazon as they battle rising gas prices.

Related: Stocks & Markets Podcast: Iran, Oil, and Volatility. How Our Profits Position Portfolios Through 2026

At the time of publication, TheStreet Pro Portfolio was long TJX, COST and AMZN.

#Wednesdays #Economic #Data #Reinforces #Bullish #Tilt #Holdings #TheStreet #Pro