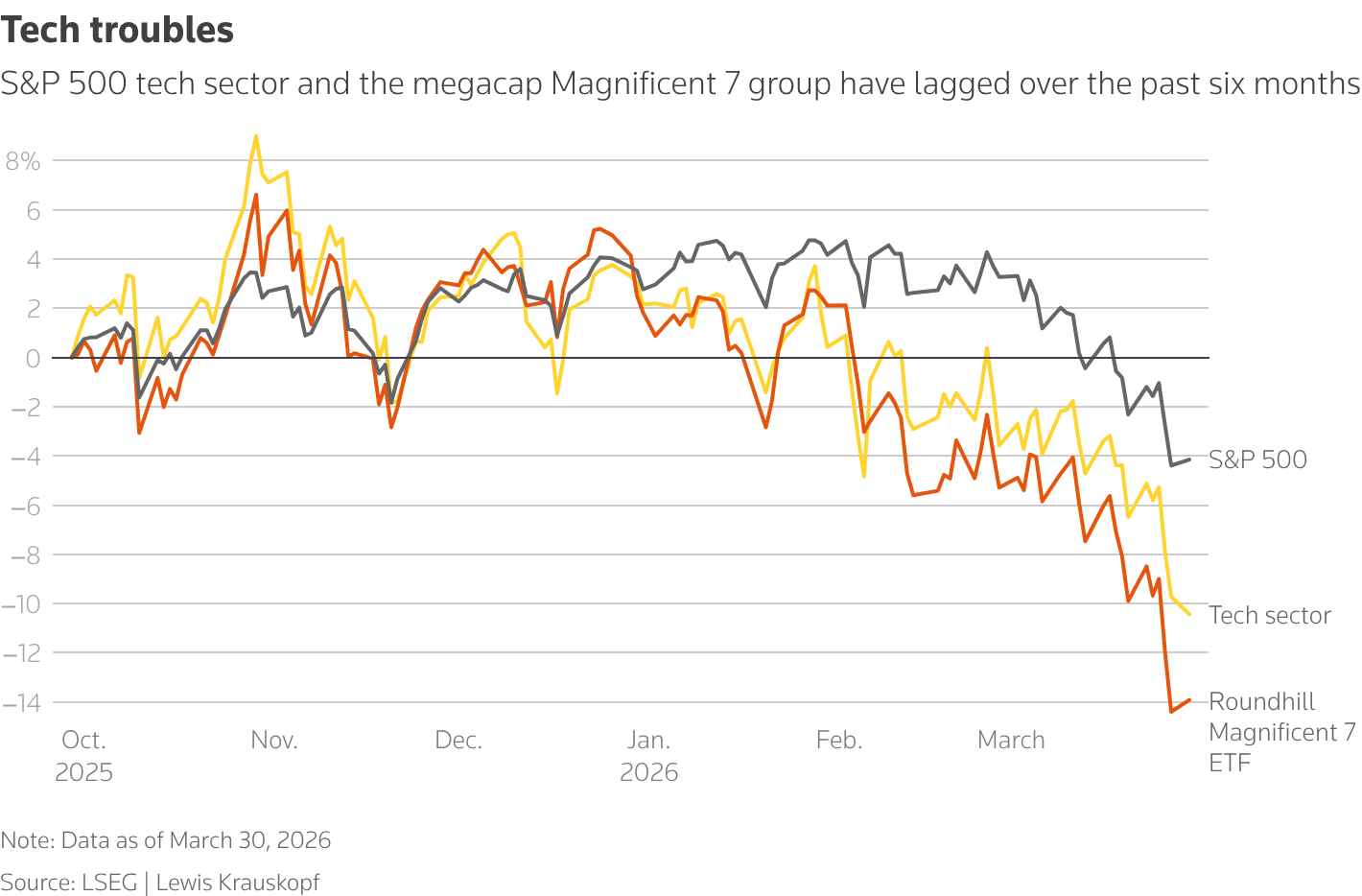

NEW YORK, March 31 (Reuters) – Technology shares are struggling to act as safe havens in the chaos caused by the Iran conflict – and that could be a big problem for the broader U.S. stock market.

Tech and other megacap technology-related stocks have driven US financial indexes higher during a bull run that has lasted more than three years, and investors are flocking to these large companies known for their strong earnings, solid numbers and competitive business advantages.

Register Here.

But the group, which had been reeling in the weeks leading up to the Middle East crisis, has sunk deeper into decline since the war began last month.

“Everything is moving forward in this environment, and so is technology,” said Angelo Kourkafas, senior global investment strategist at Edward Jones.

ACHIEVING MONEY, INSTALLING INDEXES, PROGRESSIVE MEMBERS

Analysts point to several factors that may contribute to the technology’s problems. As investors seek to reduce their equity risk, they may invest in their biggest bull market winners, including high-tech names.

“They’ve been very successful for three years,” said Walter Todd, chief investment officer at Greenwood Capital in South Carolina. “Maybe people are taking a little risk on those names, where they’ve made a lot of money.”

Rising Treasury yields, driven by inflationary concerns caused by the war, tend to offset asset prices, mostly technology stocks that are considered highly valued in terms of their future prospects.

It makes it more difficult to want to use money to work,” said Matt Orton, chief market strategist at Raymond James Investment Management.

“Because of the dominance and success of megacaps over the past few years, I think they’ve been the first and easiest source of income for investors,” Orton said. “You have this perfect storm that’s providing a strong wind for megacap technology and technology, broadly speaking.”

Such “pressure risk” means that stocks continue to influence the direction of the broader market.

“Until these big tech names can find some stability in the market, it’s going to be difficult for the broader market to find its footing,” Orton said.

TECH IS STILL PROFITABLE, WHILE THE COSTS ARE NECESSARY

Tech and megacap companies generally have good profit prospects. The technology sector is expected to post earnings growth of 43% through 2026, versus an increase of 18.8% for the entire S&P 500, according to LSEG IBES.

That earnings power will be particularly attractive if higher energy prices stemming from the Iran war hurt the broader U.S. economy, said King Lip, chief strategist at BakerAvenue Wealth Management.

“Investors will be hungry for earnings growth in a growing market,” said Lip.

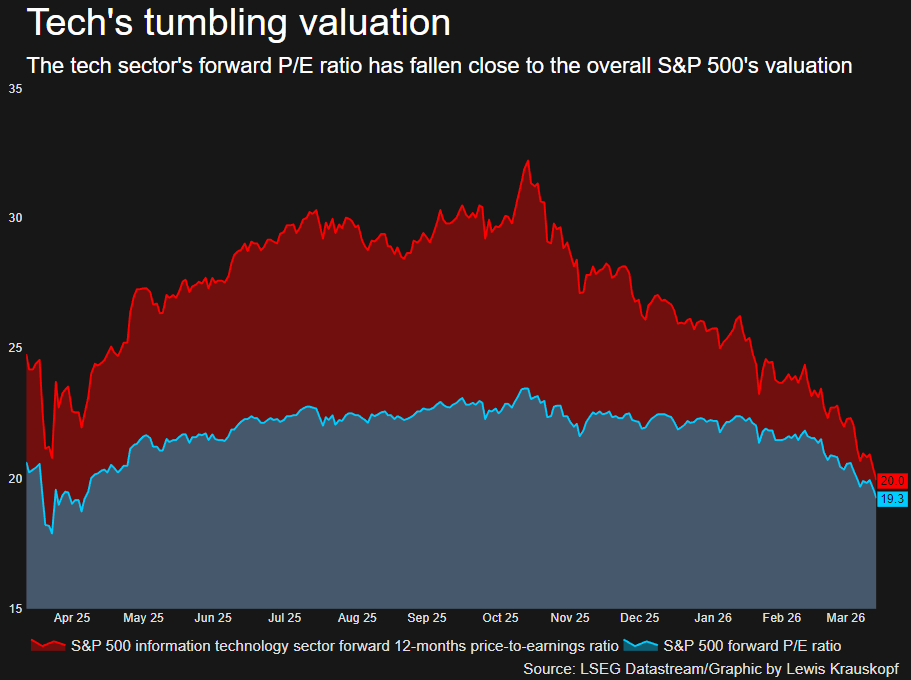

Tech’s slide also made its value even more attractive. The technology sector’s price-to-earnings ratio, based on earnings estimates for the next 12 months, fell from 32 in late October to 20 as of Friday, according to LSEG Datastream.

The average S&P 500’s P/E ratio stands slightly lower, at 19.3 times. The technology sector’s P/E ratio was about to fall below the broader market for the first time since 2017.

“The risk premium is improving,” said Chris Galipeau, senior market strategist at Franklin Templeton. “As asset prices go down, the risk of owning them goes down.”

Reporting by Lewis Krauskopf; Additional reporting by Sinéad Carew; Edited by Megan Davies and Daniel Wallis

Our standards: The Thomson Reuters Trust Principles.

#tech #stocks #struggle #find #safe #haven #Irans #stock #market #collapse