Rising mortgage rates threaten to wipe out the home buying season.

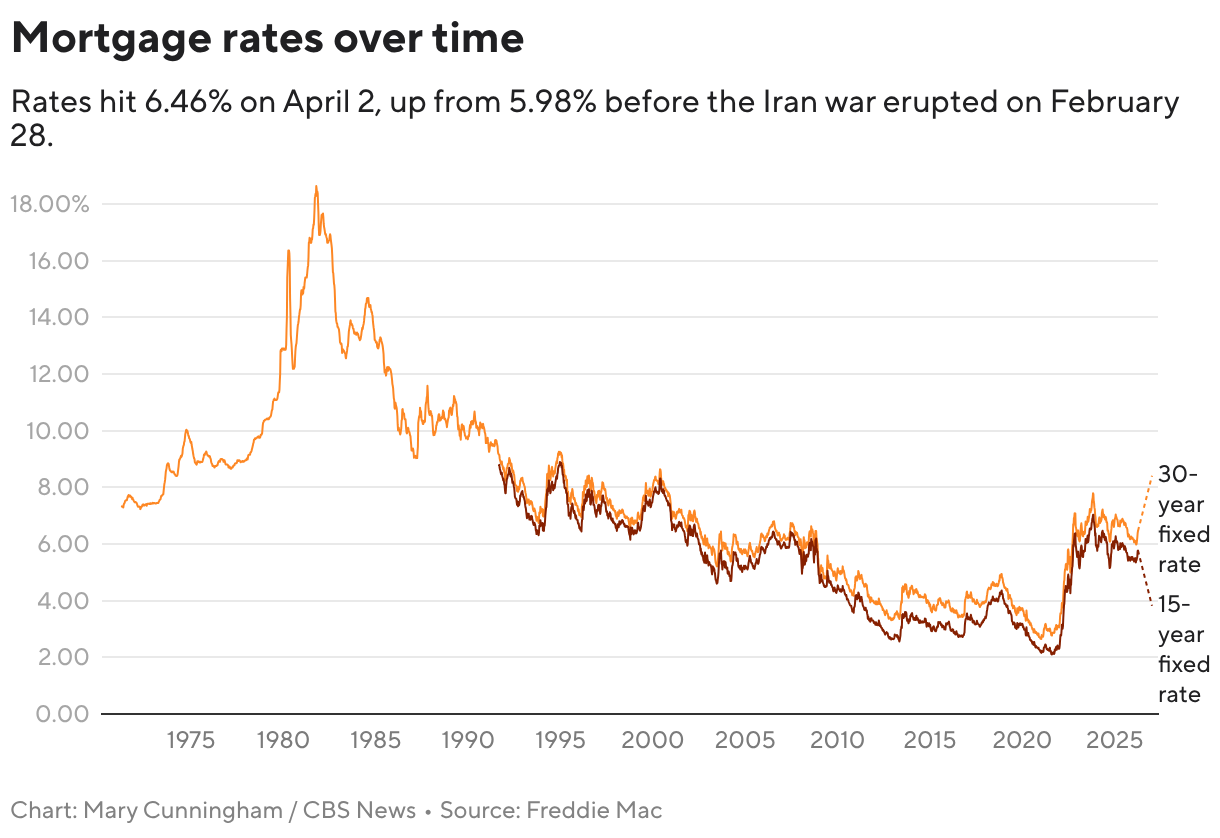

The average 30-year mortgage rate rose to 6.46%, the highest level since September 2025, Freddie Mac said Thursday. Borrowing costs have risen sharply in recent weeks following the divestment less than 6% in late February. The Iran was there it increases price pressure by raising inflation concerns and raising government bond yields, according to economists. Mortgage rates tend to track the 10-year Treasury bond.

For aspiring homeowners, rising borrowing costs are a major headache.

Rachel Marks, a 41-year-old resident of Brooklyn, New York, who recently started looking for a house, said: “Before this war, it would be a good time to buy. Now it’s like, no, stay away because everything is going up, up, up.”

As of Thursday, the 10-year Treasury yield was 4.26%, up from 3.96% before the US and Israel attacked Iran on February 28.

“When inflation rises, debt investors – and that includes mortgage-backed assets – want higher returns to compensate them for that increase,” explained Mike Fratantoni, chief economist at the Mortgage Bankers Association (MBA), a trade group.

Monetary policy guidance is also weighing on the housing market, Fratantoni said. By inflation seems to have stopped above the Federal Reserve’s annual target of 2%, a growing number of economists and Wall Street analysts are now predicting that the central bank will refrain from lowering its interest rate throughout 2026.

“Credit rates will remain high, above 6%, in part because markets have high expectations for long-term rates,” economists with PNC Financial Services predicted in a report this week.

$95,000 difference

Prospective home buyers are now facing the impact of an unexpected jump in mortgage rates.

Devan Post, a 36-year-old business executive from Minnesota in the market for a home that offers more space for his family, in February thought he had found a property that ticked all the boxes.

The lender initially quoted him a rate of 5.85% for a 30-year loan, he told CBS News. But before she and her husband could rush to propose, war broke out in Iran. Lenders’ latest rate: 6.49%.

Post and her husband recently put an offer on another house. As they get closer to buying, he said some of the loan costs they face are daunting.

“You feel like you’re finally going to get into the market when things are going your way. Like, the rates are finally going down, we can afford to buy a nice house,” he said. “And then it’s like, oh, wait, don’t care.”

If a couple locks in 6.49% and puts 20% down, they’ll pay $265 a month compared to last month’s lowest price, according to Realtor.com. That comes to $95,400 over the life of the 30-year loan.

Low season?

Higher mortgage rates coincide with the start of the home buying season, when demand begins to increase. Experts had predicted a strong start to the year, pointing to moderate inventory growth, a pace of new construction and year-over-year price declines.

The housing market was also eager to turn a page from last year’s buying season, when President Trump’s “freedom day” tariffs stoked fears of inflation and recession, according to Jake Krimmel, senior economist at Realtor.com.

“This was going to be the year that the market came back in a noticeable way,” he told CBS News. “Conditions were setting up for better prices.”

However, high debt levels have marred the picture, with Oxford Economics noting in a recent report that the impact of the Iran war on the housing market “may send many buyers and sellers on the sidelines.”

The Mortgage Bankers Association recently lowered its outlook for real estate because of what it expects to be weaker demand.

“Last month, our forecast for 2026 was for an 8% increase in real estate compared to 2025. Now we want a 5% increase,” said Fratantoni.

Krimmel said it’s too soon to tell whether higher mortgage rates will reduce housing demand, noting that “nothing is bright yet.” In some cases, rising mortgage rates may encourage people to jump on offers to lock in a good deal before costs rise, he added.

However, other indicators point to a slight decrease in demand. The MBA’s seasonally adjusted purchase index, which tracks the number of mortgage applications for new and existing homes, fell 3% on April 1 from the previous week.

#Mortgage #rates #rising #destroying #welllaid #plans #home #buyers