The economic consequences of the war in Iran continue to dominate the headlines. Investors follow their playbook and rush to the “apparent” winners in the Middle East turmoil.

For example, there are high oil prices. Last month, the following energy companies performed well:

- Exxon Mobil rose 12.44%

- Chevron rose 12.82%

- Shell rose 15.42%

- Santos rose 17.75%

- Woodside rose 18.51%

However investors looking at the market because of the current problems and opportunities created by the political turmoil we find ourselves blind.

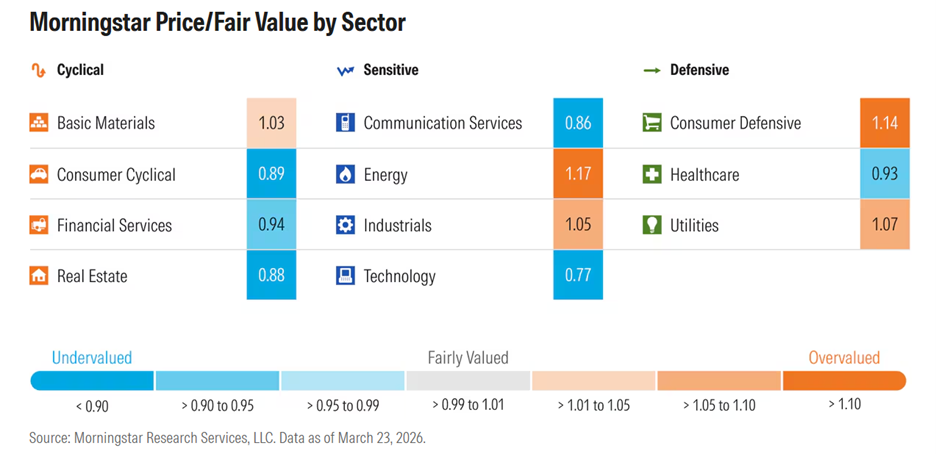

Long-term funds are driven by the mismatch between values and prices. The following chart shows the price to fair value in the US market according to our analysts.

The cheapest branches are the most despised in our current environment. The Technology and Communications sectors are affected by fears about the impact of AI. Inflation concerns continue to dampen activity in the Consumer Cyclical sector.

Those low prices do not mean that there are no reasonable problems. AI is disrupting the strong initial moats of many leading companies in the software space. As the war continues, major supply chains are being affected. As COVID has shown this can drive inflation which is difficult to control.

The reports may be true. But investors have historically overreacted to both top and bottom reports. The constant drumbeat of headlines reinforces this trend.

It’s easy to invest using the first line of thinking – for example, very expensive oil is good for oil sectors and bad for consumer spending. It is very difficult to stay several steps ahead of our current situation.

What you should do now

Successful investors will focus on where the world will be in 10 years. That is not easy but it beats trying to translate every tweet from the White House.

Remember that when investors are worried and instead of uncertain they tend to make bad decisions. Much of the advice from more sober commentators is to ‘don’t panic.’ This makes good sense and is meant to help.

But people in general are not afraid. Instead, people allow themselves to make decisions that harm their long-term interests. We describe investors as capitulating. However, no one could describe their actions as arrogance. And that separation between how people perceive their own actions and how they interpret the actions of others is important.

Stocks are influenced by the timing of buying and selling decisions. The difference between investment and investor returns is an indication of how poor we are at making decisions. Every wrong decision is a point of failure. The average has been a 1.10% gap between investment returns and investment returns over the past ten years in the latest Morningstar. Beware of the Gap study. Collectively investors are not up to the challenge in good time.

Since this is an annual study, the size of the gap will change each time we run a new data set. Over time we have noticed many trends. The gap widens if there is greater volatility. This is evident when different types of investments have different levels of volatility – say share ETFs and bond ETFs. The investor gap is greater for share ETFs than for bond ETFs. It is also evident that different periods have different levels of change.

For example, in 2019 the gap was close to 1%. In 2020 with turbulent markets in response to COVID the gap widened to 2%.

There is a lot of room for error in times like these. Reduce your thinking and analyze each decision more than you normally would. It may be a reward in the long run.

Mark LaMonika

Also in this week’s edition…

From 1 July 2026, large pension gaps will increase due to indexation. Julie Steed defines variable and fixed thresholds and thresholds.

Inflation continues to worry investors and policy makers. Michael Collins examines how central banks are rethinking inflation targets.

As data mining capabilities have increased and AI has advanced, investors have sought to identify factors that lead to alpha or underperformance. Larry Swedore reviews research that shows a new perspective is needed for investors looking to generate high returns.

Many investors believe that a “balanced” portfolio is the best of all worlds. But Werner du Preez he believes that the hidden danger of persecution may lie beneath.

Investors are fleeing bonds given higher inflation forecasts and a hawkish response by the RBA. Phil Strange sees some benefits for investors who are willing to lock in attractive returns.

The only thing that matters is the return that ends up in your pocket. Emma Davidson looks at after-tax returns on LICs and the potential for LIC issuers to provide more transparency for investors.

Joe Wiggins examines the impact of decision-making from “situationalism” when investors lose the long-term perspective while focusing on each successive short-term risk.

This week’s white paper from the World Gold Council looks at the role of gold in 2026 for Australian investors.

Edited by Mark Lamonica and Leisa Bell

Latest updates

PDF version of the Firstlinks Newsletter

Monthly Investment Podcast by UniSuper

ASX Listed Bond and Hybrid rate sheet from NAB/nabtrade

NTA Investment Company (LIC) Listing Report from Bell Potter

Updates and announcements on the Sponsor Noticeboard on our website

#Firstlinks #Edition